AI chip leader and stock market darling Nvidia (NASDAQ: NVDA) has rapidly shed over 20% since becoming the world’s most valuable company just weeks ago. Investors should think twice before rushing to buy the dip. Nvidia’s stock appreciated to breathtaking heights and the company’s once-presumed dominance of the AI chip market is now less certain.

Nvidia enjoyed rampant growth these past 18 months but relied on a small handful of customers for it.

News recently came that tech giant Apple, which will soon roll out AI tech for iOS devices, trained its AI models on Alphabet‘s AI chips instead of Nvidia’s. It’s a crack in the idea that Nvidia, which owned as much as 90% of the AI chip market, would continue to dominate without meaningful pressure from competition.

Investors may be better off letting more air out of Nvidia and circling back after its upcoming Q2 earnings give a glimpse into the business’s performance.

Instead, consider these two high-quality companies using AI to enhance their existing products. Their growth comes at solid prices, setting the stage for great long-term investment returns.

This software juggernaut offers growth at a reasonable price.

Salesforce (NYSE: CRM) is no stranger to the technology sector. The company was a pioneer in the software-as-a-service (SaaS) business model. It sells the world’s leading customer relationship manager (CRM) software but has vastly expanded over the years to form a software ecosystem packed with tools for running virtually all aspects of a company. Salesforce has been public since 2004 but remains a growing company today; the company’s business segments, sales, service, platform/other, and integration/analytics all posted double-digit year-over-year growth in Q1.

Over 150,000 companies use Salesforce worldwide, rich soil for growth via product cross-selling. Today, most revenue growth comes from expanding business with existing customers. As companies use more Salesforce products, it makes it harder to switch. Salesforce isn’t an AI-driven business, but it uses AI to enhance its products. The company launched its Einstein 1 Platform, an AI product that enables customers to use AI across Salesforce’s software ecosystem. Einstein can automate processes, deploy generative AI features, analyze and streamline data, and more. Ideally, Einstein will maximize the experience using Salesforce software, which ultimately makes customers less likely to leave and more likely to spend more.

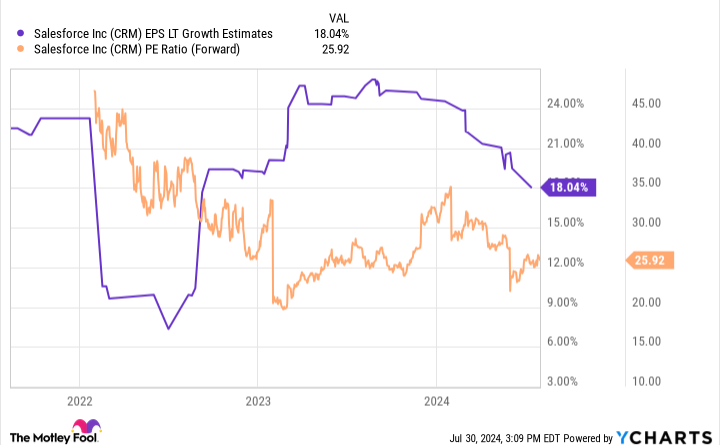

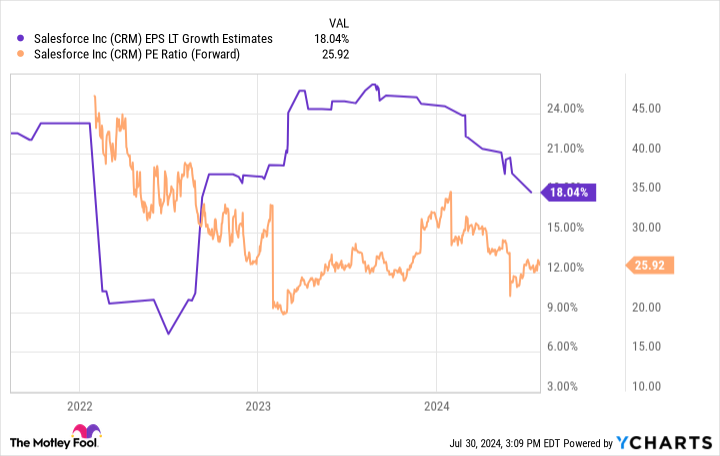

There are signs that Salesforce is a maturing company; management began share repurchases a couple of years ago and initiated a dividend earlier this year. That signals to Wall Street that Salesforce makes more profits than it needs and can’t think of a better way to spend them than simply returning them to shareholders. Analysts have also lowered their long-term earnings growth estimates over the past year:

Story continues

CRM EPS LT Growth Estimates Chart

Although the stock doesn’t look as cheap, given lowered growth expectations, its PEG ratio of 1.4 is still reasonable for long-term investors. Anticipation is building for interest rate cuts, which could plant seeds for increased growth in the technology sector over the coming years. Salesforce could realistically outperform current expectations, making the stock look cheap in hindsight. When it comes to proven winners like Salesforce, it can pay not to get too cute.

This AI stock is a stand-out rebound candidate.

UiPath (NYSE: PATH) has taken its lumps. The stock has fallen 85% from its former high, and its most recent quarter was disastrous, with the CEO abruptly resigning. Co-founder and former CEO Daniel Dines has reassumed the role for now. UiPath specializes in business automation software that learns and replicates repetitive computer tasks. It’s the type of story about machines replacing humans you don’t see in the movies. UiPath’s technology has routinely garnished leadership status from third-party testing like Gartner‘s prestigious Magic Quadrant system.

However, UiPath is clearly experiencing some challenges. The company’s Q1 earnings included layoff announcements and a scaling back of its annual recurring revenue guidance from $1.725 billion to $1.730 to $1.660 billion to $1.665 for its fiscal year 2025. Management cited several excuses, including economic conditions, deal scrutiny, and the leadership change. It smells like the company didn’t execute well under CEO Rob Enslin, who had been Co-CEO since 2022 but the sole CEO for only a few months.

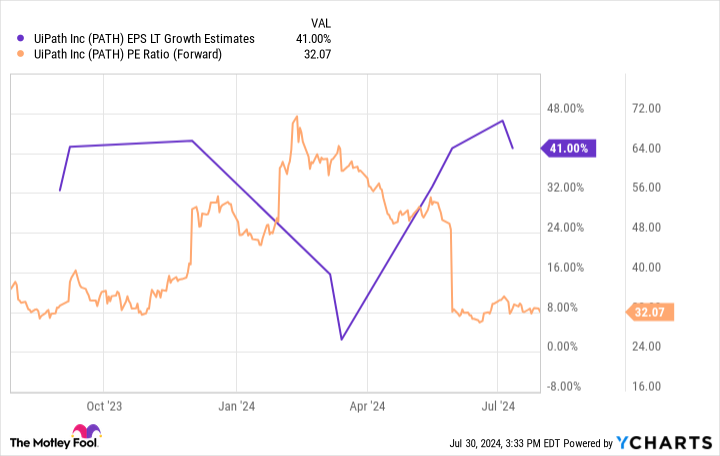

Daniel Dines has served in the CEO/Co-CEO role since 2005, so his return has seemingly restored analysts’ confidence. Long-term earnings growth estimates plummeted after Q1 but have virtually rebounded to where they were entering the year:

PATH EPS LT Growth Estimates Chart

However, the stock has not come back. Today shares trade at a forward P/E ratio of 32, which would make it a jaw-dropping bargain if UiPath delivers earnings growth on par with estimates. Annualized 40% earnings growth is a tall task, and UiPath must still prove it’s back on track. But investors who believe in the former CEO’s leadership could be staring at a rare buying opportunity today.

Should you invest $1,000 in Salesforce right now?

Before you buy stock in Salesforce, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Salesforce wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $657,306!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of July 29, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Justin Pope has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Apple, Nvidia, Salesforce, and UiPath. The Motley Fool recommends Gartner. The Motley Fool has a disclosure policy.

Forget Nvidia: 2 Artificial Intelligence (AI) Stocks to Buy Now was originally published by The Motley Fool